ML-02 Using Applications to Manage Money

This lesson discusses planning and budgeting, use of online banking services, online classified markets, making payments and receiving money electronically, and utilities including calculator. Participants will be exposed to opportunities and risks associated with online banking and trading application services, and develop awareness on how to securely use such services.

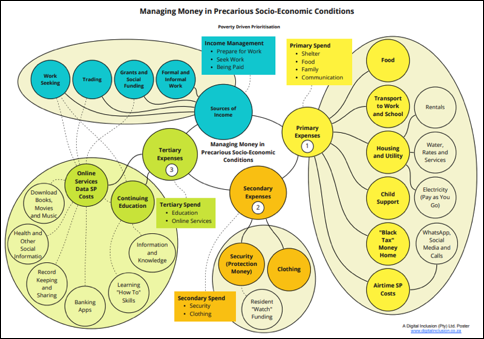

A major challenge for Elderly Adults, is how they go about managing money in their precarious socio-economic conditions. There are a number of key considerations:

- Sources of Income

- Prioritisation of Expenses

Sources of income

Income can be derived in a number of ways.

- If employed, income can be regular or sporadic, depending on whether employment is permanent, contracted or casual. Formal and informal work can generate income. Improving earnings is based on improving one’s job related competency levels and understanding, as well being able to effectively “sell” your value to employers or customers.

- Trading, either as an ad-hoc activity, or as a self-employed ongoing activity can generate income

- Social grants, and family support, are a form of income, not typically adequate in terms of sustainability. May meet basic needs only.

- Work seeking, formal or informal, is a key focus for income generation.

- In whatever way one is focusing on improving income levels, self-improvement and development is key to maximise one’s chances of success and effectively seeking work and earning appropriately for the value of services you deliver.

Prioritised Expenses

The figure presents multiple expense categories grouped as:

- Primary Expenses – Paid first, “must pay”, typically every month, meet today’s needs

- Secondary Expenses – Paid second, required but may have to be delayed if no funds

- Tertiary Expenses – Only if money left over, longer term impact, improve future (self-development), or quality of daily life (entertainment)

With limited funds coming in, and high demands in terms of expenses, budgeting and financial discipline is key. The figure below presents relative emphasis on both income and spending areas and how prioritisation of spend with limited income is potentially addressed.

Sample financial applications

When considering financial applications, there are a number of activities to consider:

- Preparing and sticking to a budget

- Calculations when buying or selling

- Keeping track of all spending

- Making sure you make payments in time

- Keeping track of any loans or investments

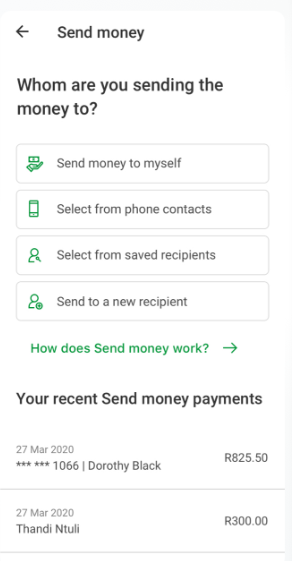

- Making payments or transfers and receiving payments or transfers from others

Some applications are on your mobile device, already installed and ready for use when purchased:

- Calculator (work out costs, profits)

- Calendar (put reminders for scheduled payments – rent, loan payments, school fees etc.)

- Notes (record keeping)

Other applications can be searched for on the Web or in the App Store (Google Play Store for Android Phones), downloaded and installed as needed:

- Budget and Expense Tracking Applications (Goodbudget)

- Financial Calculators for loan calculations (various)

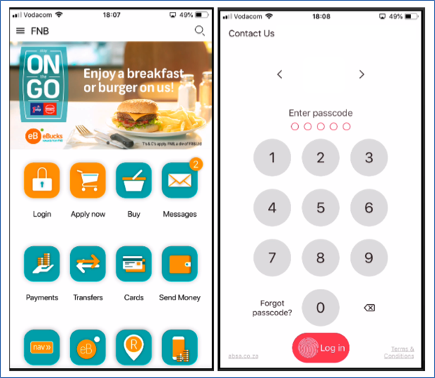

- Online Banking Applications (Capitec, FNB, ABSA, Capitec…) – you need the one for the bank where your account is held.

- Keeping copies of receipts and purchase records for warranty (Scanning application and Note Storage)

- Transfer Cash to Anyone with a phone (Online Banking “cardless” payments – Cash Send)

- Receive cash from others via your phone (SMS from Banking Apps)

If you are running a business:

- Payment Applications (Online banking for EFT – electronic funds transfer and payments)

- Payment Applications – For paying merchants (Zapper, SnapScan)

- Receiving Payments – Let others pay you with a credit or debit card (DPO Paygate, Zapper, SnapScan)

Budgeting and calculating

Using applications that offer budget management and tracking of spending, it is possible to improve financial planning and the management of risks associated with money.

In the figure above, two examples of financial tools are shown:

- Goodbudget is a free tool that manages money using a tried and tested “Envelope Method”. Like in the real world where one could put physical cash in envelopes for specific purposes, you can now do this online, with spend tracking, budgets etc. The good part of this is you can access your records on your mobile device using an application you download from the application store, or you can sign on from any web browser on any device.

- All mobile devices have a calculator pre-installed. This can be used to do any financial calculations you need. If you prefer, you can download calculator applications with more functionality from the application store.

Online banking

In the figure above, one shows the flexibility and range of services offered. The other shows methods of logging in and proving your identity. Examples of authentication verification include the use of Passcodes, fingerprints, facial recognition, and two factor authentication where two checks are done. Banking applications provide rich features. You can keep track of your accounts, review transactions, manage limits, receive alerts and notifications, and send money. You can even send money to people who do not have bank accounts. You can buy airtime and other services.